4 Budgeting Practices That Harm Your Small Business

These days, there are many different ways to become an entrepreneur. There are entrepreneurs with a brick-and-mortar establishment, those that operate a virtual business, and those who do both. There are people who make money from home full-time and those who keep their day job while managing a business on the side.

The wide array of tools and platforms available made it possible for 28.8 million small companies to start their own business – something that only a few years ago was incredibly difficult for your average office worker.

However, while selling and marketing technologies continue to evolve, budget planning strategies for business don’t seem to progress as much. If studies are any indication, small business owners have yet to appreciate the importance of budgeting as part of creating a solid business plan. As a result, the harbor and practice budgeting strategies are outdated and even harmful when applied today.

Small Business Finance Statistics You Need to Know

A budget outlines a company’s financial and functional goals. Because it gives companies a rough idea of how much money they can spend, a budget helps entrepreneurs formulate a cost-reduction action plan to improve the flow of cash too.

In order to create a budget that works, you need to know some important facts and figures about small business finance so you can make better, well-informed decisions. Here are some small business statistics you need to know:

- 60% of business owners are not confident about their financial knowledge (Small Business Report – Accounting)

- 30% of startup companies regard accountants as trusted advisors (ICAS)

- 45% of entrepreneurs are unaware that they have a business credit score; 82% of those who do cannot interpret their score (Nav)

- 30% of companies fail because of insufficient funds (CB Insights)

- 50% of labour costs are reduced by cloud computing (Forbes)

- 15% of revenue growth has been evident in companies that use purely cloud-based accounting (Xero)

- 1 in 6 loans from Small Business Administration fail (Nerd Wallet)

Just like any aspect of a business, you should only plan your budget when you have all the relevant information. You need to be able to adjust your budget easily when unexpected expenses hit, so a full picture of your company’s finances is essential to budget planning.

Another important step to remember before planning your budget is to track your spending. This will help you see patterns in your cash flow and make budgeting a lot easier. Finally, it’s also important to get rid of budgeting practices that could be harming your company. Here are 4 budgeting practices that can harm your small business.

Taking on bookkeeping and accounting tasks yourself

Many entrepreneurs do their own bookkeeping and accounting in a bid to save money. This comes as no surprise because for one thing, doing these yourself lets you gauge the financial health of your company. For another, outsourcing it to someone seems impractical when you’re just starting out.

The problem is that bookkeeping and accounting affect many vital aspects of a business. These tasks also entail a certain set of skills and a degree of expertise that most entrepreneurs don’t have. Even if you have some accounting background, it’s really more efficient to delegate this responsibility to a professional. After all, with your other obligations as a business owner, you won’t have enough time to do business accounting.

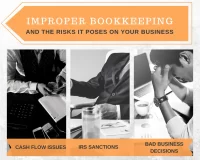

Need further convincing to delegate your accounting and bookkeeping? Consider these possible consequences of improper bookkeeping:

- Cash Flow Issues

Your financial system must clearly show how and where money flows in and out of your business. Problems occur when entrepreneurs don’t know how to track their progress in terms of profit or where their money is actually going. In fact, the cash flow problem is the number one reason why startups fail and it can be caused by improper bookkeeping practices.

Every transaction – from payments to earnings – must, therefore, be recorded, filed, and studied accordingly to avoid cash flow issues.

- IRS Scrutiny

Being audited by the IRS is an alarming prospect. The best way to prepare – and spare yourself from unnecessary worry – is by making sure that all your financial records are in order. If there are mistakes in your records, you risk paying exorbitant fines, hurting your cash flow, and damaging your credibility as a business.

- Ill-informed Business Decisions. Imagine shelling out a large amount of money for investment, only to struggle to make ends meet. Though your intention was to advance your company, you end up doing the opposite because you failed to see the repercussions of your decision. That’s what happens when you have an imprecise knowledge of your financial situation.

Designing and executing complex cost-cutting techniques

A significant part of budgeting is knowing how to reduce operating expenses in business. As easy as this sounds, it can go wrong due to improper planning and goal setting. When the bills pile up, entrepreneurs often resort to severely slashing overheads and cutting off resources without considering their overall effect on operations.

The process of cost reduction must complement the way you do business. If it’s forced, it will be hard to implement and even harder to maintain. Be wary of sources telling you to drop a certain service or switch to a different supplier without even considering its effect on your brand identity, employees, and customers.

Analyze your cost-cutting ideas and the way they fit into your goals and company vision. You don’t need to overhaul your brand or start from scratch for the sake of following trendy cost-reduction methods.

Setting financial plans in stone

Entrepreneurs who have been in business for a few years are often guilty of this mistake. When you’ve been in the industry for a while, you learn what works and what doesn’t. You already have an inkling of what this month will bring or how that season will go. At the start of the year, you already map out your finances, purchases, and expected revenue without hesitation. While tenure in business comes with many advantages, it often leaves entrepreneurs inflexible in terms of financial planning.

“Prepare for sunny days and rainy days, but don’t decide your outfit just yet,” as the saying goes. Let your experience help you brace for slow months, but don’t let it hinder you from considering other possibilities. Financial planning tends to be more convenient the longer you are in business. But when convenience turns to complacency, you expose yourself to financial vulnerability.

Budgeting for the sake of budgeting

Just like any other branch of business, financial planning should be done with clear, realistic goals in mind. Entrepreneurs sometimes regard budgeting as a task that they just need to get over and done with. This approach will lead to ineffective financial planning.

Every decision and action you make in business should ultimately lead towards adding value to your brand – and budgeting is no different.

Just consider the following scenario:

The holidays are coming. You need extra pairs of hands for marketing assistance, customer service, and administrative support. However, you also need to consider inventory costs. Would you:

- Hire onsite employees through recruitment platforms. You can always cut deals with suppliers to reduce spending on your inventory. After all, you need manpower more.

- Get extra help by asking for recommendations from friends or current staff. If you don’t work with third-party recruitment, you can save on hiring and employment costs. Plus, terminating employment would be easier this way.

- Hire a virtual assistant (VA) through a staffing agency. Remote staffing works for other companies. Surely, it will work for yours, too.

Of course, the most suitable solution would be option C. Working with a virtual staff provides business solutions with terms that won’t break the bank. It’s a smart way of allocating funds without compromising output. On the contrary, you add value to your brand when you work with credible and experienced VAs.

Honing your selling and marketing knowledge is important – as is continuously developing your financial skills. Follow these budgeting tips so your financial system propels your brand instead of holding it back.